Recession indicators, inflationary prices, stagnating growth — what do we call this?

By late January, the holiday season is finally far enough behind us to allow for a degree of analytical distance. The urgency has faded. Inventory has cleared. Earnings calls have been digested. The headlines have moved on. What remains is something rarer than immediate reaction: the ability to look backward with context, rather than adrenaline.

And when we do, the story of the economy — and of the beauty industry in particular — becomes far less straightforward than the celebratory framing that dominated December’s post Black Friday jubilation.

The dominant narrative, repeated across financial media and brand communications alike, is one of resilience. Consumers, we are told, are “still spending.” Holiday sales “beat expectations.” The feared slowdown did not arrive. Beauty, once again, proved itself defensive, durable, and culturally indispensable.

Yet this optimism sits uneasily alongside lived experience: persistent price increases, shrinking order volumes, rising dependency on discounting to generate sales, brand closures, layoffs, and a growing sense among consumers that cost no longer corresponds to value.

This tension is not accidental. It is structural.

The Duality of the Moment: Growth and Breakdown, Simultaneously

We are living through an era defined by economic duality — a condition in which success and failure are not sequential, but concurrent.

On one side of the narrative spectrum is the rhetoric of revival: America is back, consumption is strong, the system is working. On the other is an unmistakable sense of erosion — of purchasing power, of trust, of stability. Both stories circulate simultaneously, rarely interrogating one another.

This duality is reinforced by the media ecosystem itself. In a capitalist economy dependent on consumption, economic reporting does not merely describe reality — it helps produce it. Confidence is not just an outcome; it is a prerequisite.

Roughly 70 percent of U.S. GDP is driven by consumer spending, making consumer sentiment a policy variable, not just a social one. If consumers believe conditions are stable, they spend. If they spend, revenues rise. If revenues rise, markets rally. If markets rally, confidence is reaffirmed. This feedback loop is not conspiratorial; it is mechanical.

As a result, macro-optimism becomes infrastructural. It is not that negative data is fabricated — it is that aggregate indicators are privileged over distributional ones, and nominal figures are emphasized over real ones.

The system cannot afford pessimism at scale. So optimism becomes the default frame.

Macro-Optimism as a Feature, Not a Bug

In the United States, economic optimism is not merely descriptive — it is structural and ideological. As a consumption-driven capitalist economy, the U.S. system depends on continuous spending to sustain corporate profitability, asset prices, and political legitimacy. In this context, macroeconomic “optimism” functions less as neutral analysis and more as a narrative requirement of the system itself.

This does not require coordinated messaging or bad-faith actors. It emerges organically from incentive alignment. Media organizations rely on corporate guidance and government data releases. Corporations depend on confidence-driven demand. Policymakers rely on sustained consumption to avoid contractionary spirals. Confidence, in this framework, is not simply reported — it is cultivated.

As a result, economic storytelling gravitates toward aggregate indicators that reinforce continuity. Headline retail sales, nominal revenue growth, and year-over-year comparisons are emphasized, while distributional realities are quietly deemphasized. Unit contraction is obscured by price inflation. Layoffs coexist with “beats expectations.” Brand closures occur alongside record quarters. These are not treated as contradictions, but as parallel truths that are rarely reconciled.

The circularity is not incidental. If consumers believe the economy is strong, they spend. If they spend, corporate earnings rise. If earnings rise, markets rally — reinforcing the perception of strength. This feedback loop is embedded in late-stage capitalist economies where sentiment itself functions as an economic variable.

But aggregate spending metrics are blunt instruments. A trillion-dollar holiday season says nothing about who is spending, how that spending is financed, or what is being foregone elsewhere. In a K-shaped economy, optimism can coexist with stagnation — and in many cases, optimism is necessary to mask stagnation.

The American economy is structurally addicted to spending. Approximately 70 percent of U.S. GDP is driven by consumer consumption, making sentiment not just an outcome, but a policy target. When spending slows, fiscal stimulus follows. Monetary easing follows. Narrative management follows.

This creates an incentive gradient: policymakers, corporations, and media outlets all benefit from sustaining the perception of economic health. Retail sales “beat expectations,” even as unit volumes decline. Inflation-driven revenue growth is framed as demand strength. Corporate layoffs are rebranded as “strategic restructuring.” Resilience is declared, even when it is narrowly distributed.

In this framework, macro-optimism begins to resemble soft propaganda — not overt, not centrally planned, but structurally aligned. It functions as a stabilizing mythos for a system that cannot politically or financially tolerate a collapse in consumer confidence.

Yet optimism at the aggregate level can — and frequently does — coexist with fragility at the micro level. For many, the result is binary: you either accept the narrative, or experience a growing sense that it bears little resemblance to lived economic reality.

Holiday Sales as Narrative Reinforcement

Holiday sales occupy a special place in this narrative architecture. They function as a symbolic referendum on economic health — a single season expected to resolve a year’s worth of uncertainty.

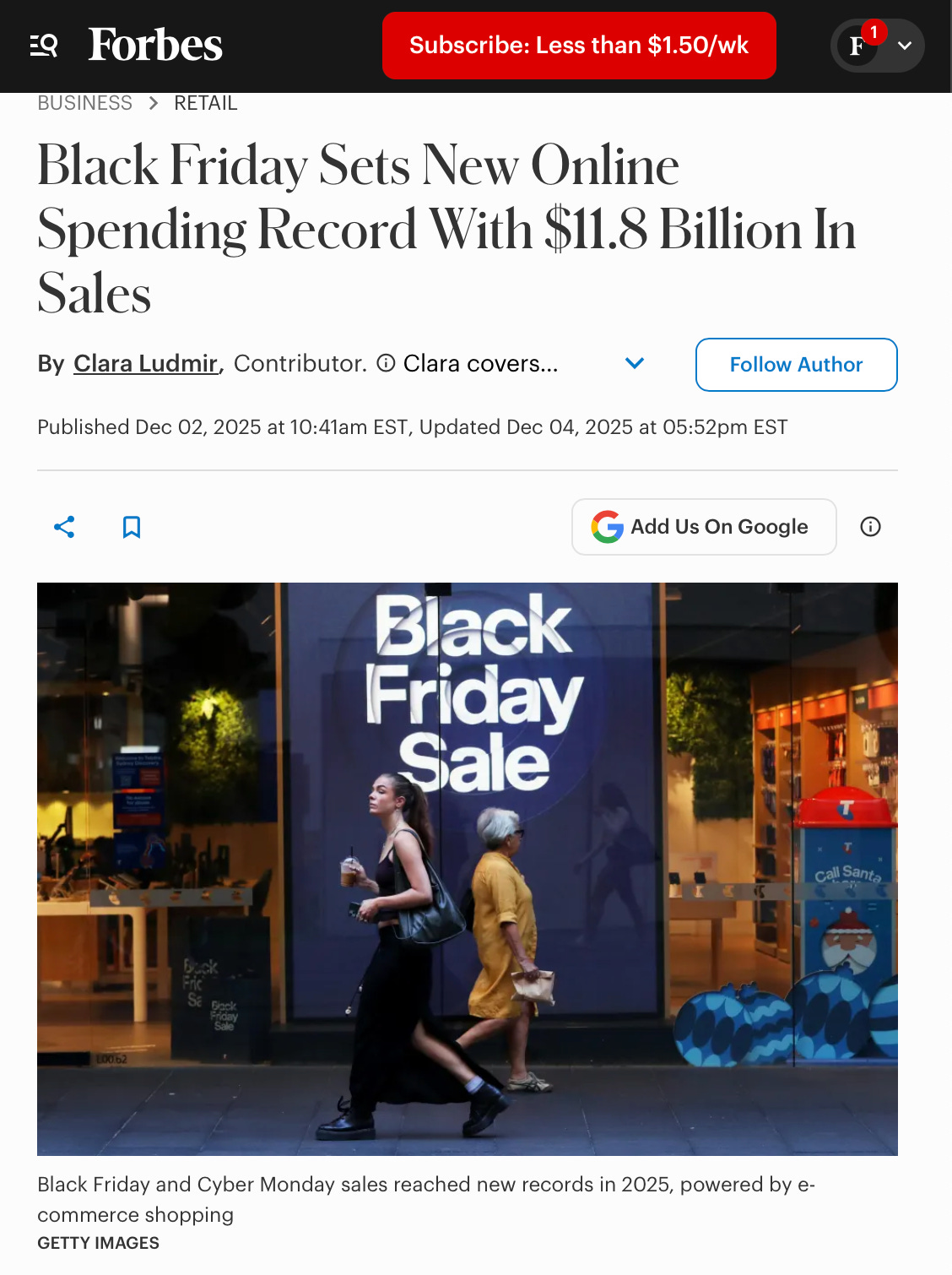

In 2025, holiday retail spending once again reached record nominal levels. Black Friday online sales rose year over year. Beauty, in particular, was repeatedly cited as a category that “outperformed expectations,” with estimates suggesting around 10 percent growth over the promotional period.

But expectations matter. That this growth was framed as a surprise already tells us something important: we were braced for weakness. A 10 percent increase was celebrated not because it was extraordinary in absolute terms, but because it contradicted a broadly anxious baseline.

This is where interpretation becomes critical.

The K-Shaped Economy, Made Visible

To understand what holiday sales actually tell us, we need to situate them within the framework economists increasingly use to describe the current U.S. economy: the K-shaped recovery.

In a K-shaped economy, different segments of society experience fundamentally different trajectories. Higher-income households — buoyed by asset appreciation, equity markets, and flexible discretionary income — continue to spend, often trading up. Lower-income households, constrained by inflation and stagnant real wages, become more price-sensitive, more selective, and more reliant on discounts. The middle thins.

Consumption does not collapse; it polarizes.

Holiday shopping patterns in 2025 reflected this precisely. High-end luxury brands saw sustained demand. At the other end, mass retailers offering deep discounts and value pricing experienced heavy traffic. What struggled was the broad, aspirational middle — brands that rely on masstige or aspirational purchasing from consumers who are neither among the wealthiest nor economically precarious.

This polarization is often misread as resilience because aggregate spending still rises. But aggregate figures obscure who is spending, how, and under what constraints.

Beauty’s 10 Percent Growth, Re-examined

Nowhere is this misreading clearer than in the beauty sector.

At first glance, a 10 percent increase in holiday beauty sales appears reassuring. But revenue growth, in isolation, is a blunt instrument — especially in an inflationary environment.

Over the past two years, beauty prices have risen sharply, often in the range of 20–30 percent, driven by higher input costs, tariffs, logistics inflation, and margin recovery efforts. When prices rise faster than revenue, growth becomes largely nominal.

In practical terms, a 10 percent increase in sales revenue under these conditions almost certainly implies flat or declining unit volume sales. Consumers are paying more, not buying more.

This distinction matters because unit growth reflects demand health; revenue growth alone does not.

Delayed Demand and Promotional Dependency

Compounding this issue is a fundamental shift in consumer behavior.

Rather than purchasing consistently throughout the year, many consumers are withholding discretionary spending until major promotional moments. Black Friday and Cyber Week no longer represent incremental demand; they function as release valves for pent-up purchasing.

This dynamic flatters holiday performance while masking broader softness. Sales appear strong during promotions precisely because consumers are not buying at full price during the rest of the year.

For brands, this creates a fragile equilibrium. Inventory clears, but margins compress. Cash flow improves temporarily, but pricing power erodes. Growth becomes increasingly dependent on discount cadence rather than product innovation or brand equity.

This is not resilience; it is adaptation.

Subscribe to get our take on the actual stories in the beauty industry.Subscribe

The Lipstick Index in a Polarized Economy

The long-standing idea that beauty is recession-proof — often referred to as the “lipstick index” — assumes a relatively even distribution of discretionary income. In a K-shaped economy, that assumption no longer holds.

Wealthier consumers continue to indulge, sometimes trading up to more premium products as a form of self-reward or status signaling (prestige perfumes have nearly doubled in price since the pandemic). Price-sensitive consumers trade down (the rise in dupes of the prestige perfumes has been the biggest growth category on TikTok), opting for mass alternatives or waiting for promotions. What disappears is the middle cohort that once sustained the heart of the economy at scale.

The result is not countercyclical strength, but fragmentation.

Beauty does not collapse — but it does not behave uniformly either. Its performance is indicative of end-stage capitalism which mirrors inequality rather than smoothing it.

Brand Closures as Structural Signals

If consumer behavior offers one lens, brand survival offers another — and it is often the more honest one.

Over the past year, the beauty industry has seen a steady drumbeat of closures, downsizing, and restructuring. These include not only small independents, but recognizable, well-distributed brands that once appeared stable.

These closures are rarely framed as economic indicators. They are attributed to strategy misalignment, overexpansion, or competitive pressure. But taken together, they point to a more systemic issue: growth is no longer sufficient to sustain the category’s breadth.

In an environment of rising costs, promotional intensity, and uneven demand, only brands with exceptional scale, capital backing, or differentiation are insulated. Everyone else is exposed.

Capital Providers Tell the Story Media Cannot

This brings us to the most revealing signal of all: capital behavior.

Consumer spending reflects what people were willing to do under pressure. Capital allocation reflects what investors believe will happen next.

If holiday sales were genuinely indicative of a healthy, durable beauty industry, we would expect capital providers to reinvest after the season. Instead, many chose to exit.

In the weeks following the holidays, Kering sold off its entire beauty division. This decision was made after the sales data was known, not before. Capital had the benefit of hindsight — and still opted for divestment.

This is not a trivial detail. Strategic exits typically occur when forward-looking fundamentals look weaker than backward-looking performance suggests. Holiday sales may have cleared inventory, but they did not restore conviction, if anything, they had the opposite effect.

Similar signals are emerging elsewhere among major capital providers, and they are far less ambiguous than holiday headlines suggest. Estée Lauder Companies has publicly acknowledged the need for portfolio rationalization, but the framing around “operational discipline” and “margin protection” masks a harsher reality: growth has become unreliable, cost structures are under pressure, and prior assumptions about beauty’s defensiveness no longer hold at scale. This is not a company optimizing from a position of strength; it is a company managing downside while searching for stability.

For others, the situation is more openly strained. Shiseido and Coty have endured prolonged underperformance with little visibility into a credible near-term turnaround. Repeated restructurings, asset sales, and strategic resets have failed to produce durable recovery, leaving both groups effectively scrambling — shrinking portfolios not because of strategic clarity, but because maintaining them has become untenable.

Even diversified giants are not insulated. Unilever has steadily retreated from beauty, treating it less as a growth engine than as a drag on capital efficiency. LVMH, often cited as proof that beauty remains structurally attractive, has nonetheless moved to reassess and selectively exit beauty assets, including Fenty — not in response to collapse, but because returns no longer justify the complexity when compared with fashion, leather goods, and hard luxury.

Internal communications at these companies have emphasized macroeconomic slowdowns, cost containment, and workforce reductions as necessary responses to deteriorating fundamentals — a notable shift from the growth-led narratives that dominated prior years. Particularly telling is the performance of once–high-growth brands within their portfolios. Shiseido’s Drunk Elephant, long positioned as a prestige growth driver, has reportedly experienced sales declines exceeding 60 percent year over year, underscoring how quickly momentum can reverse when pricing power erodes and consumer trade-down accelerates.

Capital is not reacting to promotions or headlines. It is reacting to margin pressure, cost volatility, geopolitical exposure, and the diminishing ability to pass price increases forward without demand destruction. Taken together, these moves do not describe a sector in quiet recalibration. They describe an industry under pressure, where leadership teams are managing erosion rather than executing expansion, and where capital is being withdrawn not because the category has failed outright, but because its growth model has stopped working. The media narrative continues to emphasize resilience; the capital behavior from those at the top tells a different story — one of uncertainty, retrenchment, and a conspicuous absence of conviction.

We go beyond the beauty headlines. Subscribe to receive new posts.Subscribe

The China and Tariff Constraint

Underlying many of these pressures is a geopolitical reality that beauty cannot escape.

Beauty is a deeply globalized industry. Packaging, components, and manufacturing remain heavily tied to international supply chains, particularly China. U.S. tariffs have raised costs across the board, contributing to price inflation that consumers increasingly recognize as disconnected from product value.

The idea that manufacturing can simply be reshored ignores economic reality. If domestic production were viable at scale, multinational conglomerates would already have moved. They have not — because the cost structure and manufacturing logistics does not support it.

Brands are left absorbing costs, passing them on, or compressing margins. None of these paths support long-term expansion.

So… What Are We, Really?

We are not in a classic recession. Employment has not collapsed. Consumption has not disappeared.

But we are also not in a healthy, broad-based expansion.

We are in a narrative-managed economy, where optimism functions as a stabilizing input even as underlying conditions diverge. Aggregate spending rises while unit demand softens. Holiday sales look strong while capital quietly exits. Brands survive — but fewer of them, under tighter constraints.

Beauty’s holiday performance did not disprove economic weakness. It revealed its fragile structure.

Consumers are still buying — but selectively, defensively, and strategically. Brands are still operating — but with thinner margins and greater reliance on promotions. Capital is still present — but increasingly cautious, uncertain, and willing to walk away.

Call it a K-shaped economy.

Call it segmented resilience.

Or call it what it increasingly feels like: an economy where growth exists, but belief does not extend evenly — and where optimism is less a conclusion than a requirement.

And in that sense, the most honest economic indicator may not be what consumers did during the holidays — but what capital chose to do once they were over. The media paints an ambitious picture of economic strength. Inside the beauty industry, the reality is far messier: underperformance, repeated restructurings, and leadership teams scrambling without a convincing path forward.

We are in a narrative-managed economy, where optimism functions as a stabilizing input even as underlying conditions diverge. Aggregate spending rises while unit demand softens. Holiday sales look strong while capital quietly exits. Brands survive — but fewer of them, under tighter constraints.

The Beauty Folio

Your content is a go-to source for me when I need information. Great work, as always!

I\’m glad you enjoyed it! Your kind words inspire me to keep creating informative content.

This post is a game-changer. I\’ve learned so much from it – thank you!

I love how your posts are always so well-structured and easy to follow. Keep it up!